Media Coverage

Southern Africa: The Next Global Fintech Frontier

By Business Day

The digitalisation of commerce is one of the defining investment themes of our generation. Globally, it has reshaped how individuals and businesses transact, reducing friction, broadening access and driving productivity.

Digitalising commerce is a universal transformation that affects every human – young or old, poor or wealthy – fundamentally changing how we engage in trade. It has unfolded at scale in markets such as India, Brazil and Egypt. Today, Southern Africa is positioned to follow a similar trajectory as reliance on cash declines, and digital payments and financial services expand. Fintechs are ideally positioned to lead the way.

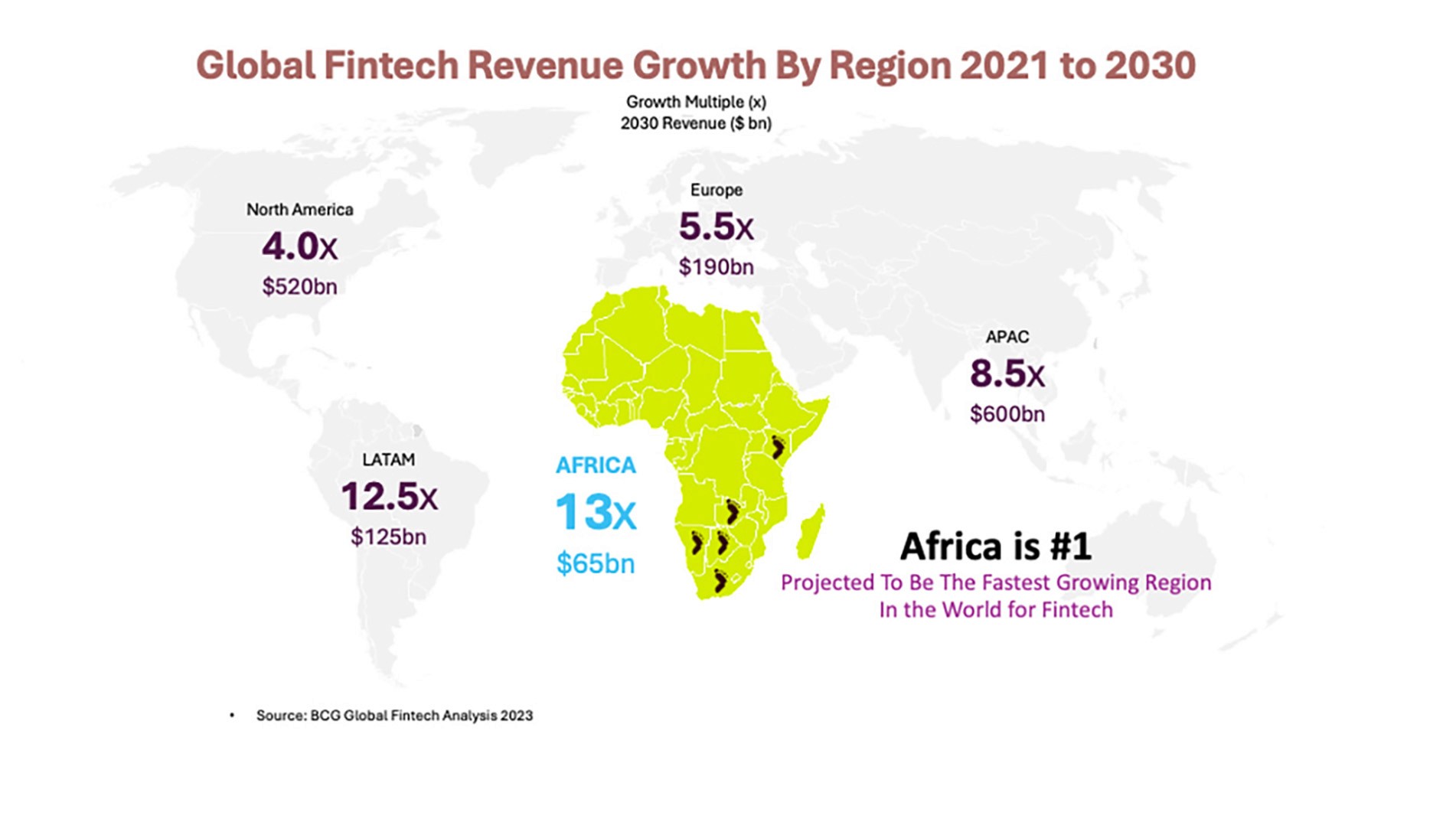

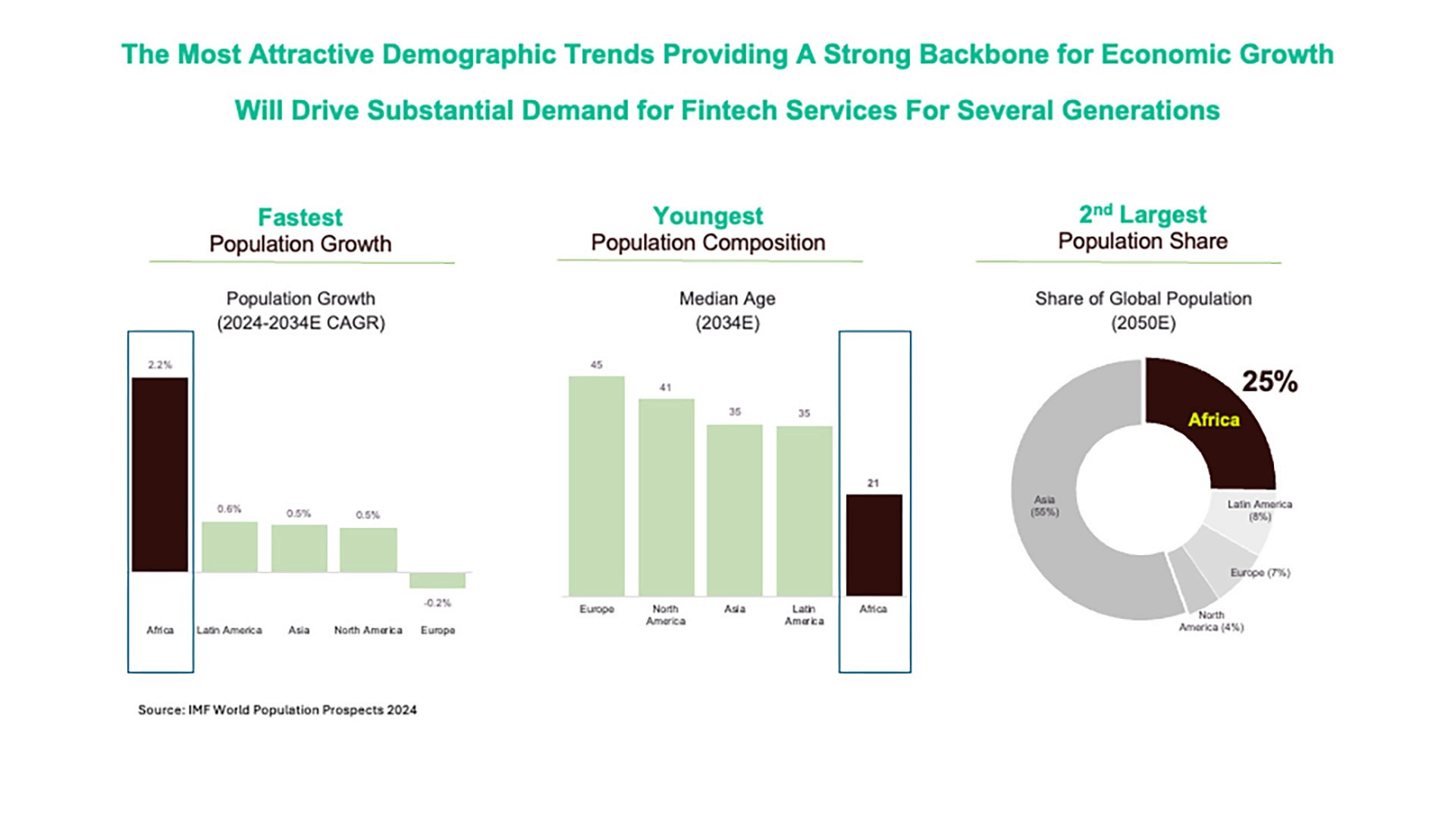

Africa is Booming: Demographic and Growth Dynamics Africa is currently the youngest continent in the world, with an average age of 21 and a population of 1.5 billion people. By 2050, Africa is projected to account for 25 per cent of the global population. From an fintech perspective, the continent is projected to be the fastest-growing region globally, with a projected revenue growth of 13x between 2021 and 2030, significantly higher than North America (4x), Europe (5.5x) or the Asia-Pacific region (8.5x).

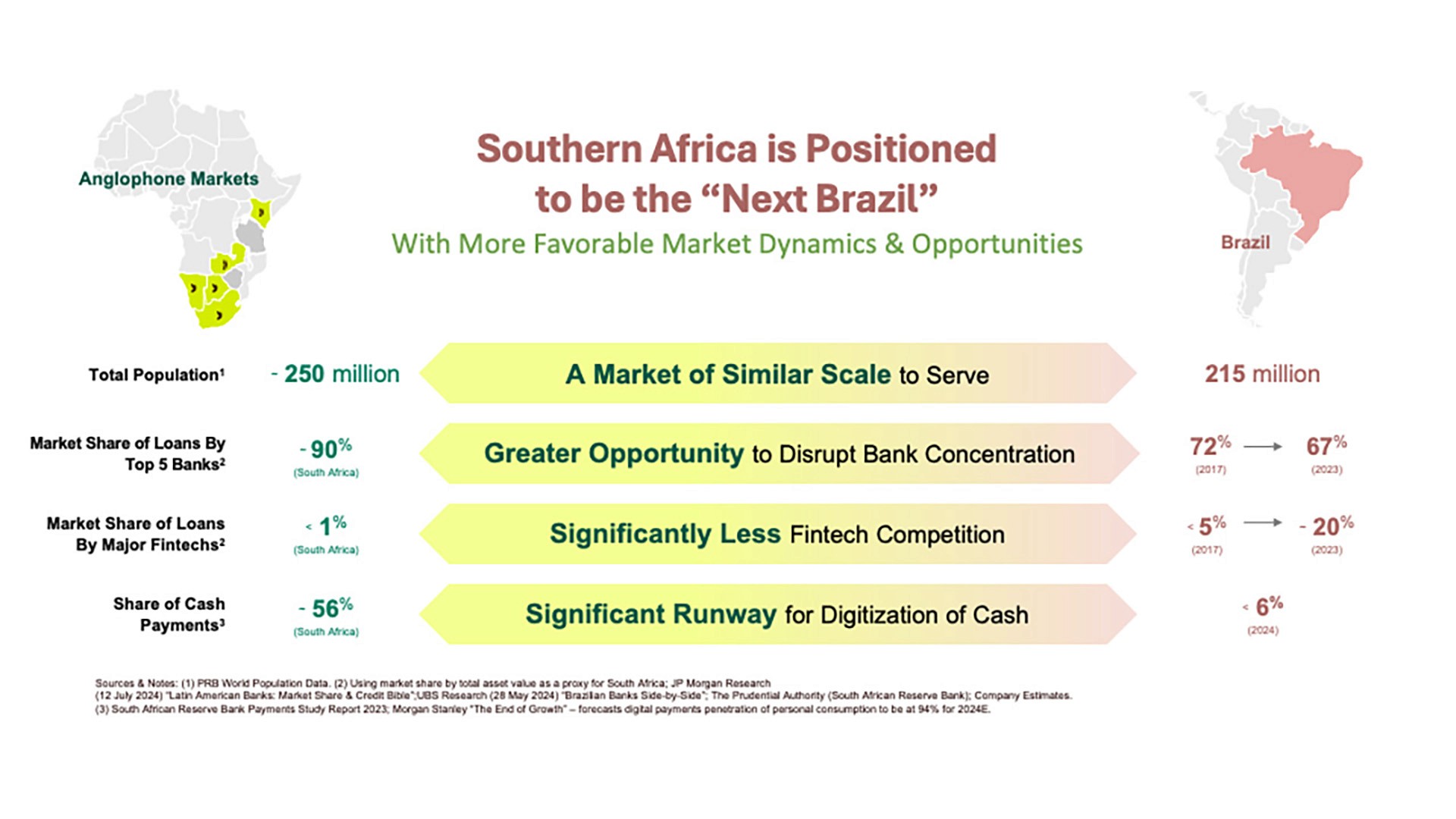

Within this context, the five markets of South Africa, Botswana, Namibia, Zambia and Kenya provide a fertile base to benefit from these long-term tailwinds. These regions represent a combined population of approximately 250 million people, a scale comparable to that of Brazil.

THE “NEXT BRAZIL”: A MARKET COMPARISON

Southern Africa bears striking similarities to Brazil’s market dynamics in 2017, before its fintech boom. Brazil’s financial services economy has transformed between 2017 and 2023. Currently, the market share of loans by major fintechs in South Africa is less than one per cent, compared to Brazil’s five per cent in 2017. However, over the course of six years, Brazil’s fintechs captured over 20 per cent market share of loans.

Companies like StoneCo disrupted banks by focusing on the underserved small and medium enterprises segment. StoneCo has grown into a unicorn with a market cap exceeding $3-billion. Agi is a fintech that combines digital and physical distribution to provide banking, insurance and credit to the most underserved populations.

It currently has over six million clients and was recently listed on the NYSE with a market cap of over $1-billion. StoneCo and Agi are not isolated success stories; Brazilian fintech now make up approximately 30 per cent of the market capitalisation of major banks. By contrast, the market cap of the top four fintechs in South Africa is less than five per cent of the top four banks. These parallels suggest substantial upside for fintech expansion in Southern Africa as it disrupts bank concentration and digitises the cash economy.

THE PARADOX OF CASH: A MASSIVE OPPORTUNITY FOR DISRUPTION

Despite high bank account penetration in South Africa, the economy remains overwhelmingly cash dominant. Approximately 56 per cent of all transactions in South Africa are still conducted in cash. Even more startling, data from the South African Reserve Bank indicates that 50 per cent of adults withdraw the entire digital deposit from ATMs immediately upon receiving it. This disconnect is most visible at the point of sale, in our transport system and in small and medium businesses. This reliance on cash acts as a regressive “tax” on society, including high handling costs and security risks, and facilitates crime. For many small traders in rural areas, traditional digital payments are unattractive due to settlement delays and material merchant fees. A merchant may often wait days for settlement, while cash provides immediate liquidity – an essential consideration for small enterprises, where cash flow is king. This structural inefficiency in the traditional banking system has created the runway for fintechs to lead the digitisation of the economy.

FINTECHS ARE IDEALLY POSITIONED TO LEAD

Fintechs are built on three core pillars that give them an advantage compared with incumbents:

1. Regulatory changes: As seen in Brazil, Southern Africa is in the process of removing traditional barriers that protected incumbent banks. For example, proposals in South Africa would allow nonbanks to participate directly in the payments infrastructure without requiring a bank sponsor. Fintechs are also playing a growing role in regulatory modernisation through ASAPP, an association of 13 nonbank fintechs.

2. Agile technology: The absence of legacy systems, combined with dynamic teams and agile operating models, allows fintechs to adopt new technologies, such as artificial intelligence and blockchain, more rapidly than incumbents, using them to drive efficiency and more authentic customer engagement.

3. A “positive sum” mindset: Fintechs are not encumbered by current profit pools and heavy cost structures, which, while significant to banks now, are at a high risk of declining over time.

LESAKA: LEADING THE DIGITISATION OF SOUTHERN AFRICA

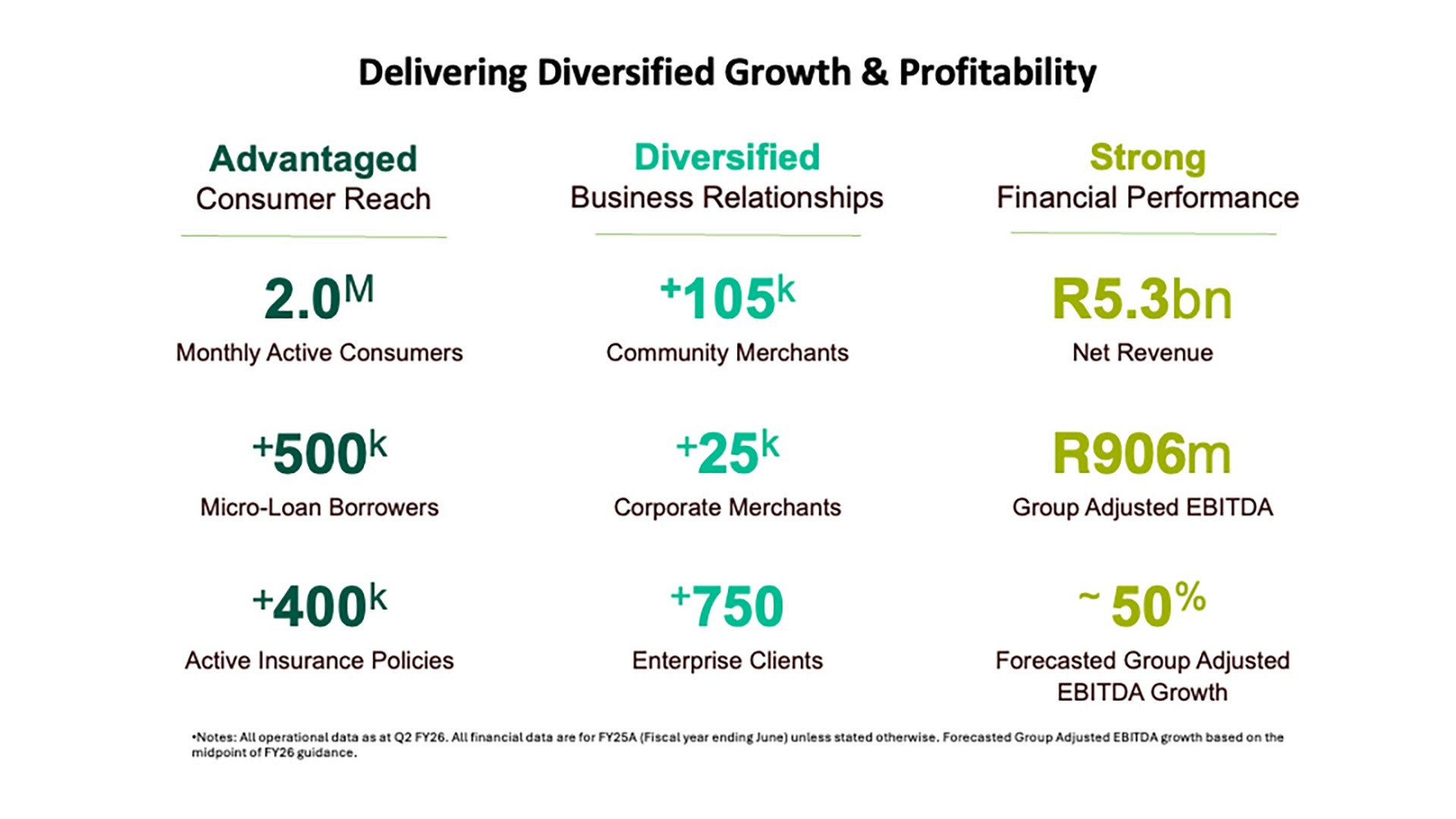

Lesaka empowers underserved Southern African consumers and merchants to fulfill their potential by delivering innovative financial services and other business services focused on meeting their needs, where they are. Over the past four years, Lesaka has established itself as among the largest independent fintechs in Southern Africa. The company has three divisions – consumer, merchant and enterprise – serving over 2 million active retail consumers, 130 000 merchants and 750-plus enterprise clients.

Consumer division: provides banking services to grant recipients, including transactional accounts, credit and insurance. Lesaka’s consumer division provides human connectivity with over 250 hyper-local hubs and over 800 local sales agents, combined with the convenience and efficiency of a digital bank. Clients are onboarded and can transact with a card in under five minutes. This division has seen a growth in active consumers from 1.4 million in Q2 FY24 to 2 million in Q2 FY26. Close to 50 per cent of Lesaka’s 2 million active clients have more than one product with Lesaka.

Merchant division: offers acquiring, software, cash management, alternative digital products and lending to small and medium enterprises, including informal community merchants – a segment traditional banks have underserved. The average revenue per merchant is approximately R1760 per month, indicating the level of incumbency. Almost half of Lesaka’s merchants now utilise more than one product.

Enterprise division: acts as a technology infrastructure provider, managing solutions for billers, utilities and municipalities. Enterprise provides bill payment services to Lesaka’s consumer and merchant clients, as well as major banks and retailers in Southern Africa. If you are paying your municipal bill through your bank app or at a retail store, there is a good chance you already use Lesaka’s services.

BOLD STRATEGIC MOVES

In 2025, Lesaka announced the acquisition of Bank Zero, a fully digital neobank, representing a significant strategic milestone. The transaction will enable Lesaka to deliver and expand its suite of financial services without reliance on a third-party bank sponsor and strengthen control over its banking infrastructure. Notably, the founders of Bank Zero demonstrated strong alignment with Lesaka’s long-term strategy by electing to receive Lesaka shares for the majority of the purchase consideration, resulting in their collective position as one of the company’s largest shareholders. This alignment underscores the partnership-oriented nature of the transaction.

Over the past decade, several digital banks have been launched in South Africa, typically requiring multibillion-rand capital investments and extended timelines – often five years or more – to achieve scale and profitability. Bank Zero offers an ultra-modern technology stack and a highly secure, low-cost banking platform, positioning it favourably relative to Lesaka’s alternatives. In turn, Lesaka brings scale, distribution and a diversified customer base, which is expected to accelerate Bank Zero’s path to sustainability within the broader group. The bank is expected to reach profitability within the first 12 months post-acquisition. Strategically, the integration is expected to reduce Lesaka’s dependence on legacy banking infrastructure and technology, broaden its reach into underserved communities and support the expansion of product offerings across deposits, lending and transactional services, particularly for small and medium enterprises. Collectively, the transaction enhances Lesaka’s capability to innovate across its ecosystem while improving operational #exibility and long-term economics. From a balance sheet perspective, the transaction is expected to reduce group debt by around R1-billion and reduce funding costs for Lesaka’s existing merchant and consumer businesses.

Lesaka is also proud to be part of a consortium that recently launched the ZARU stablecoin (ZAR-pegged stablecoin). Powered by the Solana blockchain, ZARU enables 24/7/365 settlement, bypassing traditional banking hours. For a merchant, this could mean T+0 (trade plus zero days) settlement velocity – instant liquidity that removes the 24- to 48-hour wait for capital – the primary barrier to digital adoption in the informal economy. For consumers, it can offer cheaper and faster cross-border payments to family and dependents.

A TRACK RECORD OF PROFITABLE GROWTH AND ACCRETIVE ACQUISITION

Lesaka is a profitable growth story with its organic and inorganic strategies clearly demonstrated in its financial performance. For fiscal 2026, Lesaka has guided to an adjusted EBITDA (earnings before interest, taxes, depreciation and amortisation) of between R1.25-billion and R1.45 billion – representing a three-year compound annual growth rate of 49 per cent at the midpoint. On a per-share basis, adjusted earnings per share have grown at over 100 per cent in the past two fiscal years, from a loss of 266 cents in FY23 to a profit of 229 cents per share in FY25.

THE NORTH STAR AMBITION

The goal for fintech in Southern Africa is to work back from the future. South African giant Naspers became the largest business on the continent by investing in the digitisation of commerce in China via Tencent – the next multibillion-dollar African champions will be those that invest in the digitisation of Africa itself.

Fintechs are the modern infrastructure – the ports and railways of the digital age. By combining disruptive distribution models, blockchain-native transparency and a deep commitment to the community, fintechs are ideally positioned to lead Southern Africa away from cash and towards a fully digitised, inclusive and thriving economy.

The journey has only just begun, and Lesaka is leading the way.