Media Coverage

Where reach meets tech: The strategic logic of Lesaka’s Bank Zero deal

By Raymond Steyn | Financial Mail

South Africa’s first wave of digital challenger banks all arrived with broadly the same pitch. Ditch the expensive branch networks, rebuild the banking architecture from a clean slate, charge little or nothing for day-to-day banking, and let the smartphone or computer become the primary interface.

On paper, the propositions sounded similar. Yet half a decade later, the outcomes could hardly be more different. One player has amassed more than 12-million customers. Another has quietly built a sizeable, deposit-rich franchise that now reaches well beyond its parent’s ecosystem. And a third — arguably the “purest” digital bank of the lot — remains stubbornly small.

That third player is Bank Zero, and its slow trajectory is a useful case study in what really drives scale in retail banking.

Bank Zero was founded in 2018 and opened to the public in August 2021, well after the concept of app-only banking had entered the mainstream. By 2025, it had about 40,000 funded accounts and just over R400m in deposits. In absolute terms, those numbers are respectable for a start-up. In relative terms, they are tiny.

Compare that with TymeBank, recently rebranded as GoTyme Bank, and Discovery Bank. TymeBank, founded in 2015 and soft-launching in early 2019, has about 12-million South African customers with roughly R8bn in deposits. Discovery, which got its licence in 2017 and began trading in 2019, has grown more deliberately to reach about 1.2-million customers and a deposit book of roughly R23bn. By any measure, Bank Zero has been left far behind.

The natural assumption is that Bank Zero simply lacked the right technology or product. Yet the evidence suggests otherwise. Its technology backbone is modern, built on a hybrid-cloud architecture and unencumbered by the legacy systems that typically slow traditional banks. The app is widely regarded as elegant and secure. The bank was designed around automation and cost-efficiency from day one. If anything, Bank Zero looks like the textbook definition of what a digital bank should be.

The catch is that banking — especially in South Africa — has never been purely a technology problem.

The first disadvantage was timing. TymeBank and Discovery both went live in 2019, before Covid and before incumbents fully responded to the threat. At the time, zero-fee or ultra-low-cost banking still felt disruptive. Early adopters were actively looking for alternatives. By the time Bank Zero launched in 2021 with a name that implicitly promised zero fees, most of the big banks had already rolled out their own low-fee or pay-as-you-use accounts.

The second, and more decisive, factor was distribution. TymeBank understood early that South Africa is not a frictionless, app-only market. Millions of customers still deal heavily in cash, lack reliable or affordable internet access, or simply prefer a physical touchpoint when opening an account. So Tyme built a “phygital” model, installing kiosks in Pick n Pay, Boxer and Foschini stores and creating thousands of merchant points for deposits and withdrawals. A customer could walk into a supermarket, scan their ID and walk out minutes later with an active bank card.

That network changed the game. It turned grocery stores into branches at a fraction of the cost, embedding Tyme directly into the daily lives of lower-income consumers. At its peak, the bank was adding well over 100,000 customers a month. About three-quarters of its base are low-income or previously underbanked people.

Bank Zero, by contrast, stayed almost entirely digital. No branches and no kiosks inside retail stores. Sign-ups were driven through its app and website. From a cost perspective, that discipline makes sense. From a growth perspective, it is brutally slow. Pure digital acquisition assumes that customers are already comfortable with self-service onboarding and remote verification. In South Africa, that assumption holds for a sliver of the market.

Discovery took yet another route. At launch, many assumed it would simply cross-sell to Discovery Health and Discovery Life clients. That was true initially, but it turned out to be only part of the story. Over time, Discovery Bank managed to attract a significant share of customers from outside its traditional ecosystem. In 2025, about two-thirds of new clients reportedly had no other Discovery product.

Discovery’s differentiation lay not in price but in incentives. Its Vitality Money programme tied interest rates, rewards and benefits to financial behaviour, echoing the group’s health insurance model. That resonated with middle- and higher-income customers who already engaged with rewards ecosystems. The result was slower customer growth than Tyme, but higher average balances — hence a deposit base far larger than Tyme’s despite having fewer accounts.

Bank Zero had neither advantage. It did not have Tyme’s mass retail presence or Discovery’s powerful rewards ecosystem and brand cross-sell. Its proposition was rational and elegant — low fees, strong security, modern tech — but without consistent, everyday visibility, it was also easy for customers to overlook.

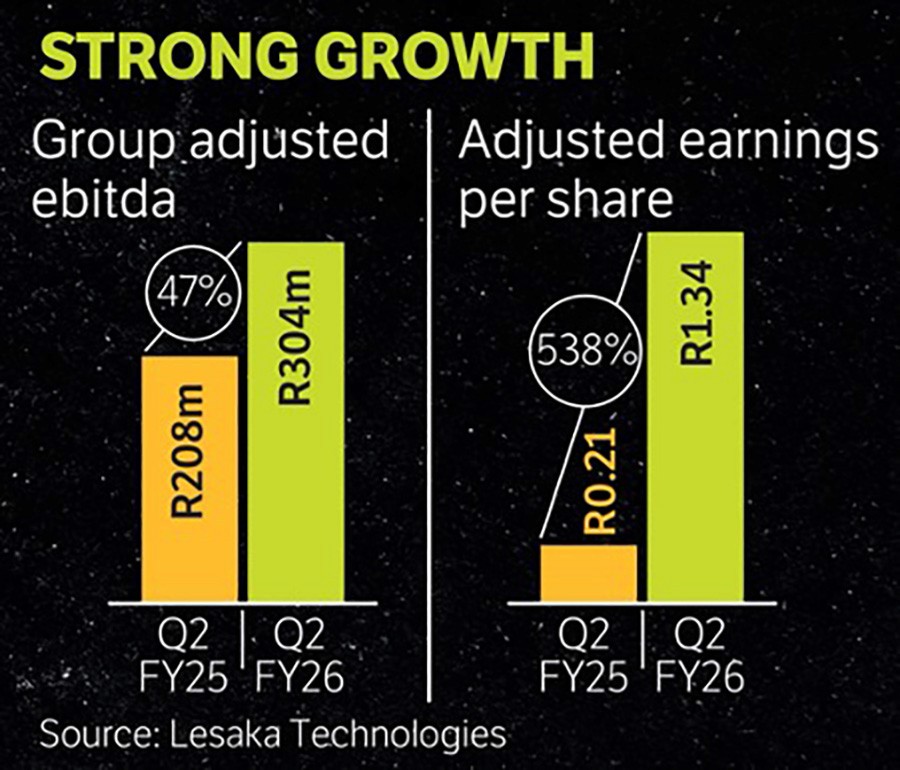

Group adjusted ebtida vs Adjusted earnings per share (lesaka technologies)

Of course, capital also matters. TymeBank benefited from deep-pocketed backers and later acquisitions that accelerated its lending and SME footprint, receiving roughly R7bn in equity injections before reaching breakeven in December 2023.

Discovery Bank, meanwhile, had the balance sheet support of its listed parent and was prepared to absorb sustained start-up losses to build scale, with close to R10bn in equity contributions before turning profitable in December 2024. Bank Zero grew far more frugally, largely self-funded by its founders. Caution preserved capital but also restricted marketing, partnerships and product expansion. In retail banking, scale is often bought before it is earned.

Put differently, Bank Zero approached the market like a disciplined engineer — focused on building a pristine system and optimising costs — while its rivals acted more like aggressive retailers, prioritising reach, marketing and rapid customer acquisition.

That dynamic, however, is set to shift with the bank’s acquisition by listed fintech player Lesaka Technologies, which brings with it the scale, distribution and commercial muscle Bank Zero previously lacked.

Ali Mazanderani, executive chair of Lesaka, declines to single out any particular fintech as the group’s primary rival, arguing that the question itself misses the point. What matters far more, he tells the FM, is the shape and size of the overall opportunity, and the reality that South Africa remains at the very early stages of challenger-bank adoption relative to comparable emerging markets. That context fundamentally alters how competition and performance should be thought of.

Ali Mazanderani: We’re only just beginning to tap into what digital can actually unlock. (supplied )

“If you look at the overall banking sector, the bulk of transactions are still running through legacy systems and a material portion of the economy remains cash-based,” he says. “We’re only just beginning to tap into what digital can actually unlock.”

South Africa’s digital-only banks, even when aggregated, account for a fraction of total banking volume and customers. That contrasts sharply with markets such as Brazil, where more than 20 digital banks have collectively captured about 45% of individuals’ primary bank account relationships — and have done so even while traditional incumbents continue to control around 70% of industry assets.

Investor favourite Nubank offers a vivid illustration of what scale can look like once adoption reaches critical mass. The fully digital, branchless bank now serves about 127-million customers across Brazil, Mexico and Colombia and commands a market capitalisation of about $81bn — a size that would have seemed fanciful for a “neobank” barely a decade ago.

Mazanderani speaks from experience. A seasoned global fintech entrepreneur, he co-founded the European payments group Teya and previously held senior executive roles at StoneCo in Brazil and Network International in the UAE. Having watched similar transitions unfold in those markets, he believes South Africa lags Latin America by about a decade, despite sharing many of the same structural characteristics: a large informal and underbanked population, significant income inequality and widespread mobile penetration.

Part of that lag has to do with history. Mazanderani points to past legislative and regulatory environments that, for long periods, favoured the incumbents and made entry and scale difficult for newcomers. Barriers included cumbersome licensing processes, complex clearing requirements and an ecosystem that prioritised stability over competition. Too often, the effect was to entrench the legacy banks and limit the flow of customers to new entrants, no matter how compelling the technology or value proposition. “Those obstacles are largely gone now,” he says, “and the market is opening up in ways that I think will unleash rapid gains for low-cost digital banking and fintech more broadly.”

That belief in the inevitability of growth is rooted in what Mazanderani sees as a simple economic truth: customers will choose lower fees and more efficient service when they are available. Digital platforms reduce a variety of charges, speed up transactions, cut friction and ultimately deliver value. In a market where many consumers are still tied to high-fee traditional banking products, that proposition should resonate widely. For Mazanderani, the question is not whether digital banks will grow, but how fast and how they will segment the market as they do.

He rejects the premise that the challengers are in a zero-sum game among themselves. “Investors should rather be looking at the vulnerabilities of the legacy incumbents,” he says, and how those institutions stack up against the new entrants collectively. In his view, the real disruption is not challenger vs challenger, but challengers vs the traditional banking model. The cost base and structure of the new digital banks give them an inherent advantage in pricing and in developing new products quickly. Those efficiencies will, over time, erode the market share of big banks that carry decades of branch networks and legacy IT systems.

In South Africa, a notable characteristic of consumer behaviour is the ownership of multiple bank accounts — even among lower-income clients. Much like in the telecommunications sector where people carry multiple SIM cards, many South Africans maintain accounts across several banks. This multibanking behaviour serves practical purposes: ring-fencing finances, separating business from personal transactions, or simply spreading risk.

“That’s actually helpful for adoption,” Mazanderani says. “When people use different cards and accounts for different purposes, they build trust incrementally. Trust leads to adoption, and adoption leads to deeper engagement.” Seen in that light, Bank Zero’s slower growth should not be mistaken for an irreversible failure to gain traction. Rather, it suggests that the opportunity is still very much intact — that market share can be unlocked as distribution improves and the bank gains broader reach, rather than the door having already closed.

Another aspect of the digital transition is the shift from simply acquiring customers to deeply engaging them. In markets such as Brazil, leading digital players no longer stop at offering a basic transactional account. They layer on savings, credit, insurance, investments and payments into a single integrated platform. That breadth of services drives higher lifetime value, strengthens customer loyalty and blurs the boundary between banking and everyday financial life. By comparison, most South African challengers are only beginning to evolve in that direction.

The prospect of building that kind of ecosystem — supported by the distribution, capital and complementary capabilities of an established fintech platform — is a key reason Lesaka Technologies opted to acquire Bank Zero, in a transaction expected to close before June 30.

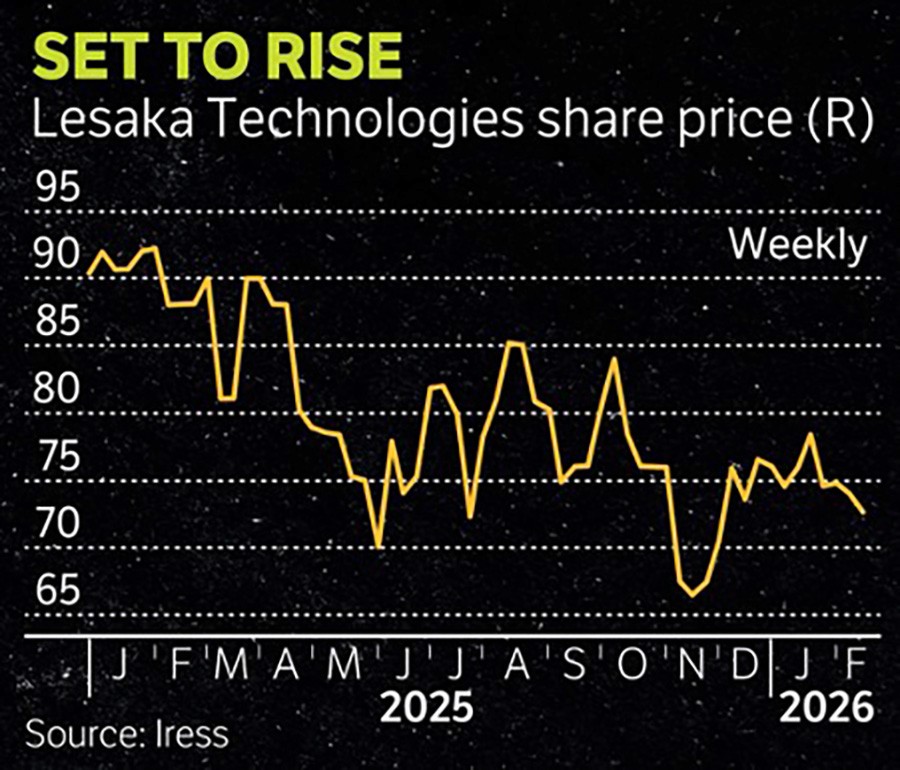

Lesaka Technologies share price (R) (Vuyo singiswa)

The regulatory path is already largely cleared. The Competition Commission has recommended that the Competition Tribunal approve the deal, signalling limited competition concerns. The final outstanding hurdle is approval from the Reserve Bank’s Prudential Authority.

The economics of the deal are straightforward. The transaction values Bank Zero at about R1.1bn and will be funded predominantly in Lesaka shares, with a small cash component. Following completion, Bank Zero’s existing shareholders will own about 12% of the enlarged group. Co-founder Michael Jordaan is set to join the Lesaka board, while Yatin Narsai will remain in place as Bank Zero’s CEO, ensuring operational continuity. Management has guided that the deal should be earnings accretive, even before considering longer-term synergies.

That matters because Lesaka, on a standalone basis, is already guiding to at least R4.60 in adjusted earnings per share for the 2026 financial year — and that guidance explicitly excludes any contribution from Bank Zero.

The most immediate benefit is funding. Until now, Lesaka has largely relied on bank facilities and wholesale funding to support parts of its lending and payments activities. By owning a licensed bank with retail deposits, it can substitute cheaper, stickier customer funding for more expensive debt. Management estimates that at least R1bn of bank borrowings could be replaced with deposits relatively quickly after completion.

But the logic of the deal extends well beyond cheaper liabilities. Strategically, it plugs directly into Lesaka’s broader operating model as a diversified fintech platform with three distinct business divisions.

The consumer division, which contributes roughly 45% of ebitda, is focused on lower-income and underbanked individuals. A large share of its customer base consists of social grant beneficiaries, and through its EasyPay platform — which commands a share of about 14% of this market — Lesaka provides transactional banking, credit and insurance products to about 2-million customers.

Before its 2022 rebrand and broader strategic reset under new leadership, the group operated as Net1 UEPS Technologies and was primarily associated with its subsidiary, Cash Paymaster Services, which for years handled the distribution of social grants on behalf of the government. That arrangement became mired in controversy and contractual disputes with the state, leaving the company with reputational baggage. Since then, the new management team has made a concerted effort to distance the business from that legacy and reposition it as a modern, growth-orientated fintech platform.

The merchant division, which accounts for about 48% of ebitda, provides card acquiring, point-of-sale devices, working capital and value-added services to more than 130,000 SMEs. Think of thousands of spaza shops, township taverns, informal traders and independent retailers who need payments acceptance, software services and short-term funding.

The enterprise segment, which contributes a more modest 7% of ebitda, connects more than 620 corporates and service providers to its digital payments platform, enabling the collection and processing of recurring payments at scale. It also operates a utilities-focused business, including a prepaid electricity management system that handles metering, vending and settlement for municipalities and other providers.

What the acquisition of Bank Zero effectively does is add the missing piece: a full banking licence and modern digital core that Lesaka controls end to end.

Until now, parts of the group’s ecosystem still depended on partner banks for safeguarding funds, settlement and regulated deposit-taking. That creates cost leakage and operational complexity. By integrating Bank Zero’s infrastructure directly, Lesaka internalises those economics and shortens the value chain, with average revenue per user (Arpu) expected to rise sharply. Product development cycles also shorten because there is no third-party bank to negotiate with and data flows more seamlessly across divisions.

In theory, that unlocks a much tighter ecosystem. A merchant using Lesaka’s point-of-sale device can be offered a Bank Zero business account on the spot. A consumer receiving wages or grants through Lesaka channels can be migrated into a full digital bank account with savings and credit. Enterprise clients can settle directly into Lesaka-controlled accounts rather than through intermediaries. Each additional service deepens engagement and reduces churn.

For Bank Zero, this is arguably the distribution jolt it has lacked since launch. As a standalone digital bank, it struggled to scale purely through app downloads. Inside Lesaka, it inherits a nationwide footprint of merchants, agents and customers. The same technology that once looked underutilised suddenly has a ready-made pipeline.

Seen this way, the transaction is less a traditional acquisition and more a convergence of two complementary models: Bank Zero’s clean, licensed banking system and Lesaka’s boots-on-the-ground fintech distribution. If Mazanderani is right that South Africa is still in the early stage of challenger bank penetration, then controlling both infrastructure and customer relationships could prove pivotal to the group’s long-term growth trajectory.

While Lesaka remains primarily focused on South Africa, its ambitions are not confined to a single market. The group has operations in several other African countries, predominantly in Southern Africa, and Mazanderani makes it clear that the long-term strategy is to broaden that footprint across the continent. While expansion may include acquisitions, he emphasises that any deal will need to be both strategically complementary and earnings-accretive before it is pursued.

The addition of Bank Zero fits neatly into that philosophy. Though often characterised as a small retail challenger, the bank has built a meaningful base among SMEs and even mid-sized corporates — precisely the types of clients that overlap with Lesaka’s merchant ecosystem. That creates immediate cross-selling opportunities. Merchants already using Lesaka’s point-of-sale, acquiring and working-capital products can now be offered fully fledged business banking accounts in-house, while Bank Zero customers gain access to Lesaka’s broader payments and lending capabilities.

The depth of the leadership bench is impressive. Beyond Mazanderani and Jordaan, the board and executive team bring considerable financial services and payments experience. Lincoln Mali, the group’s Southern Africa CEO, previously headed the card and payments division at Standard Bank Group. CFO Dan Smith brings a capital markets lens, having served as an investment partner at Value Capital Partners — Lesaka’s largest shareholder — and on the boards of JSE-listed PPC and AdvTech. Steven J Heilbron, head of corporate development, adds deep banking and dealmaking credentials, having previously been joint CEO of Investec Bank plc and having played a key role in the development of Connect Group.

Given that backdrop, the market’s current scepticism looks somewhat puzzling. Despite the strategic logic of the acquisition and the prospect of cheaper deposit funding, Lesaka’s share price has drifted 17% lower over the past year. The stock trades on an undemanding forward earnings multiple of 16 — and that excludes any earnings uplift from the Bank Zero deal.

Mazanderani, careful not to comment directly on the share price, falls back on the familiar line: “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.” Still, actions often speak louder than words. In December, he personally acquired about $9m worth of shares, a tangible vote of confidence in the group’s long-term trajectory. The caveat for local investors is liquidity: with most of the register sitting on the Nasdaq, trading volumes on the JSE can be thin.

In a low-growth South African economy, where many of the more compelling listed stories tend to come from businesses that disrupt or consolidate traditional sectors, fintech remains one of the few pockets of genuine structural expansion. And with Lesaka still carrying some legacy scepticism from its past, the valuation may offer patient investors an attractive entry point into that theme.